CBI nabs GST superintendent, inspector in bribery trap in Chennai – The Times of India

CBI nabs GST superintendent, inspector in bribery trap in Chennai The Times of India

CBI nabs GST superintendent, inspector in bribery trap in Chennai The Times of India

Vijayawada: Barber Receives Rs 72 Lakh GST Notice For Iron Scrap Business Deccan Chronicle

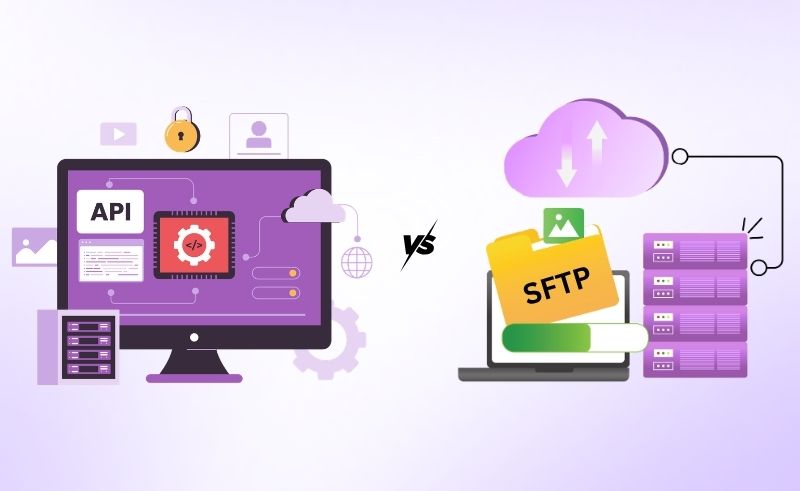

The average GST invoice moves through hundreds of touch points across the organization and beyond. Its journey begins from an ERP and then travels through integration layers to reach the Invoice Registration Portal and return with an IRN. The GST invoice then flows into reporting systems and audit trails where transmission of regulated financial data is transmitted thousands of times each day in large enterprises. However, large enterprises often overlook these facts about invoices while designing their GST compliance infrastructure. They tend to exclusively focus on automation or reporting capabilities. As a result, the integration layer that carries compliance data between enterprise systems and GST networks receives far less attention. That layer quietly determines something far more important than convenience. It determines how securely tax data moves across the enterprise stack. For example, if a large FMCG company generating 50,000 invoices daily relies on delayed batch uploads, it is doing so at the risk of missing compliance timelines. As GST adoption expands across India, this architectural decision is becoming increasingly important. The Expanding Scale of India’s E-Invoicing Ecosystem India’s e-invoicing framework has blown up far beyond what it was planned for. When the current system was first introduced, the mandate was applicable only for the handful of India’s largest enterprises. However, the revenue threshold has reduced in phases over the last few years pulling more businesses within the compliance network. Today, the GST infrastructure is overwhelmed with more than 13 lakh GSTINs transmitting invoice data throughout the compliance network. The turnover threshold has dramatically changed where organisations with an annual turnover exceeding ₹5 crore are required to comply with GST compliance requirements that were once applicable only for companies with more than a ₹500 crore annual turnover. The evolution of the e-invoicing mandate clearly shows how rapidly the ecosystem has expanded, with the eligibility threshold gradually reducing over the years. Today, compliance requirements are more stringent that ever before. Businesses with turnover above ₹10 crore are required to submit invoices on the Invoice Registration Portal within 30 days of the invoice date. Invoice data is typically transmitted over TLS-encrypted channels to the Invoice Registration Portal (IRP) via GSTN APIs. These developments have increased the volume and frequency of data transmission between enterprise systems and GST infrastructure. As a result, the integration layer that carries this data has become a critical part of compliance operations. Two Ways GST Data Typically Travels to the GST Network Most automated GST environments rely on one of two integration approaches. SFTP uses SSH-based encryption to secure file transfers in transit. SFTP-based integration In this model, enterprise systems export invoice or return data as files. These files are transferred through secure file servers before being processed and submitted to GST systems. API-based integration In an API architecture, enterprise systems communicate directly with GST infrastructure through secure request-response connections. Each transaction moves as structured data in real time rather than through batch files. Both models enable GST automation. The difference lies in how data flows through the system and how securely that information travels across the integration pipeline. Data is typically transmitted over TLS-encrypted channels to the Invoice Registration Portal (IRP) via GSTN APIs. How SFTP-Based GST Integration Works Since file transfer mechanisms have been the staple for enterprise system integrations, initially GST automation followed the same pattern. Here’s how a typical SFTP workflow looks like. The ERP systems generated invoice data and converts it into either a JSON or CSV file format. The file is then uploaded to a secure file transfer server from where a compliance platform retrieves it to process the data and sends it to GST systems for validation. This approach works well for batch processing environments where data moves at scheduled intervals. Many organizations implemented their GST infrastructure using this model during the early adoption phase because it aligned with traditional enterprise integration methods. However, as transaction volumes increase, operation complexities occur within file-based pipelines. Before a transaction file is sent to the GST network, it must be created, transferred, monitored, and processed. Heavy transaction volumes create a strain on the file-based mechanism where delays or failures become unavoidable. Where File-Based Transfers Introduce Security and Operational Risk SFTP is widely considered secure because the file transfer channel itself is encrypted. However, the broader workflow includes several stages where sensitive compliance data may exist within the integration pipeline. Key operational and security considerations include: Multiple intermediate storage points GST data is usually generated as files before transmission. These files may temporarily reside in export directories, SFTP servers, or processing systems before reaching the GST network. Expanded data exposure surface Every additional storage location becomes another point where invoice data, tax information, and customer details exist within the system environment. APIs reduce storage-based exposure but introduce runtime security considerations such as endpoint protection and rate limiting. Credential management complexity File transfer environments frequently rely on shared authentication credentials across systems. Managing access controls and credential rotation across these systems can become operationally demanding. Delayed error detection Batch processing means issues during file generation, or transfer may only become visible after the batch cycle completes, which can delay corrective action. These characteristics do not make SFTP unsuitable. Many organizations operate stable file-based systems successfully. However, as invoice volumes increase and compliance timelines become stricter, organizations often evaluate architectures that minimize intermediate handling of sensitive data. How API Based GST Integration Changes the Architecture API-based integration approaches the problem from a different direction. Instead of generating files and moving them across servers, enterprise systems communicate directly with GST infrastructure through secure API endpoints. When an invoice is generated inside the ERP, the system sends a request containing the transaction data to the GST network. The Invoice Registration Portal validates the request and returns the IRN response. This exchange happens within seconds. The process becomes a direct system-to-system interaction. There are no intermediate files and no scheduled transfer cycles. APIs do not store data. APIs themselves are communication interfaces, but underlying systems may temporarily store logs,

Rising maintenance costs, GST charge hit gated communities hard The Times of India