GST return filing becomes predictable or painful long before anyone starts preparing GSTR-1 or GSTR-3B. The difference lies in how data moves inside the organization during the month, and not in what happens on the filing date.

In many businesses, GST compliance looks orderly on the surface. Returns are filed on time. Portals reflect acknowledgements. Yet internally, teams operate with constant caution. Numbers are reviewed repeatedly, GST return reconciliation stretches into filing windows, and approvals multiply as deadlines approach. Over time, GST return filing becomes less about compliance and more about reassurance.

This is not because GST rules are unclear. It happens because return filing depends on data assembled from multiple systems ERPs, billing tools, adjustment workflows that were never designed to stay aligned without integrated GST return filing. As volumes increase, that gap widens quietly.

This article explores why GST return filing becomes operationally fragile at scale, and how integrated GST return filing automation restores alignment between transactional data and statutory returns.

For example, a credit note issued after month-end may reflect in ERP revenue adjustments but miss the GSTR-1 extraction cut-off. The result surfaces weeks later as a GSTR-1 vs 3B mismatch, even though the transaction itself was valid.

The Pressure Inside GST Return Filing Operations

GST return filing relies on two outcomes that must stay aligned every month. GSTR-1 captures outward supply details at an invoice level. GSTR2B captures Inward supply details (auto-generated inward supply statement (not a return)) GSTR-3B consolidates tax liability at a summary level. All originate from the same business activity, yet they often rely on different data treatments by the time they reach filing.

Operationally, this is where friction starts. Invoice data flows through ERPs, billing platforms, adjustments, and credit notes before reaching returns. Small differences in timing, classification, or rounding rarely attract attention when transactions occur. They surface later, during reconciliation.

Why GST Return Filing Grows More Complex as Organizations Scale

At lower volumes, finance teams can rely on experience and manual oversight to maintain alignment. As organizations grow, this approach starts to strain.

Multiple business units contribute data. Amendments accumulate across periods. Adjustments move closer to month-end. GST returns depend on extracts taken at specific points in time, rather than on continuously aligned datasets.

As a result, GST return reconciliation then moves to the back end of the process. Teams discover mismatches after most numbers are already prepared. Corrections feel rushed. Explanations rely on memory rather than traceability.

This is where GST return filing consumes disproportionate effort in growing, ERP-based organizations. The problem does not sit with people or processes. It is the absence of system-level coordination between transactional data and automated GST(1) compliance workflows.

How Integrated GST Return Filing Automation Changes the Process

Integrated automation addresses GST return filing at its foundation. It connects systems instead of patching outcomes.

Rather than treating GSTR-1 and GSTR-3B as separate exercises, automated GST compliance ensures both draw from synchronized data. Validation rules apply while data moves, not after filing pressure peaks. GST return reconciliation becomes part of the workflow, not a corrective exercise.

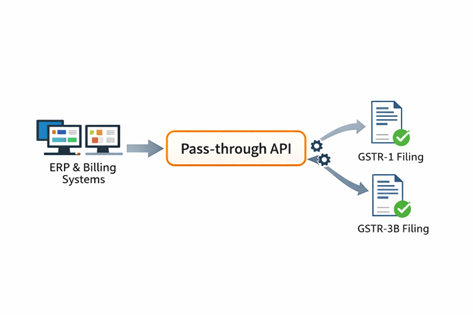

A GSP API for GST return filing plays a key role here. APIs maintain structure as data passes between systems. They reduce format reinterpretation. They allow validations to happen consistently across returns.

This approach does not alter how businesses transact. It changes how transactions translate into compliance.

(Also Read: Best E-Invoicing Software Built for ERP Integration and GST)

How this Transformation Shows up in Day-to-Day Operations

The first visible shift appears in filing readiness. With GST return filing automation teams know days in advance whether data is aligned. Reviews happen with context rather than urgency. Filing timelines feel manageable because the system has already done most of the alignment work.

GST return reconciliation stops dominating the calendar. When mismatches appear, teams trace them quickly because data lineage remains intact. Adjustments feel controlled rather than reactive.

Audit preparation also changes character. Questions about filings get answered with traceable records instead of reconstructed logic. Confidence improves because data tells a consistent story across returns.

As volumes grow, effort does not grow at the same pace. Integrated automation absorbs complexity quietly. Teams retain oversight without expanding manual checks.

What Integrated Automation Delivers in Real Terms

When GST return filing moves through an integrated GST return filing automation layer, the benefit does not show up as a flashy dashboard or a shorter checklist.

It shows up in how calmly teams operate during filing cycles, how predictable outcomes become, and how fewer surprises surface after submission.

The value sits in consistency, traceability, and control across volumes, entities, and periods. Over time, this changes how leadership views compliance, shifting it from a recurring operational risk to a managed system capability.

Measurable Benefits of GST Return Filing Automation

Sustained data consistency across returns

Integrated automation ensures that outward supply data, tax liability, and summary values originate from the same transaction base. GSTR-1 and GSTR-3B reconciliation stay aligned by design, not by correction. This reduces exposure to mismatches that often surface weeks later during notices or internal reviews.

Early visibility into filing readiness

Filing preparedness becomes measurable days before statutory deadlines. Teams see where gaps exist while there is still time to act. This avoids last-weekend reconciliations and creates a predictable close cycle for indirect tax.

Controlled reconciliation instead of firefighting

Reconciliation shifts from a post-filing activity to an in-flow check. When differences arise, they appear with context: source record, system touchpoints, and transformation logic. This shortens resolution time and prevents repeat issues in future periods.

Reduced dependency on manual interpretation

Validation rules apply uniformly as data moves through systems. This limits subjective judgment during filing pressure and reduces errors caused by format conversions, spreadsheet logic, or version conflicts.

Improved audit confidence and response quality

Automated lineage allows teams to respond to audit queries with evidence rather than explanation. Data trails remain intact from ERP entry to filed return, strengthening defensibility without additional effort.

Scalable compliance without proportional headcount growth

As transaction volumes increase or entities expand, the compliance process absorbs complexity without adding layers of manual checks. Oversight remains centralized while execution stays stable.

By standardizing invoice data, organizations also experience smoother GSTR-1 reconciliation, reducing last-minute filing delays.

Reduced compliance volatility across periods

Filing outcomes become consistent month after month. Variance reduces, rework declines, and leadership gains confidence that GST compliance will not disrupt broader financial operations.

The Role of Excellon Exact in GST Return Filing Automation

Excellon Exact functions as a pass-through SAP-certified GSP API solution. It does not replace ERP systems or filing software; instead, it acts as a reliable conduit, ensuring that GST data flows seamlessly from enterprise systems to the GST portal.

By maintaining the structure and integrity of transactional data during transmission, Exact reduces the risk of errors caused by format conversions or manual interventions. It validates data as it passes through, helping GSTR-1 and GSTR-3B reflect the same underlying business activity without altering how businesses operate internally.

This approach is particularly suited for organizations that prioritize system alignment and audit defensibility. Exact enables GST return filing to remain predictable and traceable, while leaving core processes untouched.

Conclusion

GST return filing will continue to evolve as transaction volumes grow and scrutiny tightens. Organizations that rely on downstream corrections will feel increasing pressure. Those that adopt integrated GST return filing automation will gain stability.

Integrated automation provides a way to simplify GST return filing without changing how businesses run. When systems stay aligned, compliance becomes predictable, and confidence returns to the process.